The true costs of credit cards

Credit cards can be a great resource when used appropriately. However, mismanaging credit cards can lead to a debt spiral that can result from the high interest charged by credit cards. Additionally, credit mismanagement can negatively impact your credit score. Which increases the costs of borrowing money for large loans such as a car loan or a mortgage. The negative impacts that can result from credit mismanagement make it extremely important that we understand the true costs of credit cards.

Understanding the true costs of credit cards

Interest rates

Credit cards advertise their APR (Annual percentage rate) which could be lower than the actual interest you may be charged if you carry a balance. If you carry a balance for more than a month you will be paying based on an APY (Annual percentage yield), which takes into account compounding interest.

A credit card may advertise a 15% APR or 1.25% monthly rate (1.25% * 12 months = 15% APR). However, if you carry a balance for a year then your actual interest rate or APY is 16.08% [(1 + 0.0125)^12 – 1 = 16.08%], as a result of interest compounding each month. Understanding this is key to knowing how much you will actually pay for keeping an outstanding balance.

Credit cards can give you a false sense of security; making you feel like you can afford things now and pay them off later. This is what has led the average american to have $38,00 in debt excluding their mortgage debt. You can avoid paying interest all together by paying your credit card in full on a monthly basis!

Minimum payments

Paying only the minimum payment is the most expensive way to pay off your credit card balance. Minimum payments are usually a percent of your balance plus interest and applicable fees. Therefore, your entire minimum payment will not go towards your balance because you will need to pay interest and other fees.

Minimum payments may come off as a way to save money now by making smaller monthly payments but it is far from that. If you continue to make only the minimum payments then interest will accrue on the outstanding balance and you will end up owing way more than you initially charged on your card.

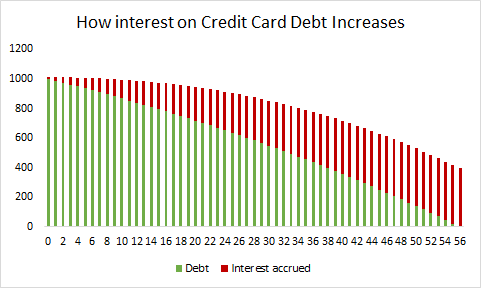

For example if you made a $1,000 purchase with a 15% APR credit card and make only minimum payments of $25 per month you would accrue about $400 in interest. That is 40% of your original purchase and it would take more than 4 and a half years to pay off! This is with the assumption that you are making no additional purchases, any additional purchases would only increase the interest you pay!

This graph represents how minimum payments can contribute to the increase of interest payments. As you can see minimum payments can be misleading and the best way to avoid paying interest is making more than the minimum payment.

Other Fees

Annual fees

These fees represent costs that your credit card charges to keep your account open. These fees usually apply to cards that offer rewards and the more benefits the credit card provides the higher the annual fee may be. The good news is that there are plenty of credit cards that do not charge annual fees so you can easily avoid them. The first card that you open should have no annual fees so that you can keep it open even if you stop using it later on because closing it will impact the average age of your credit.

Late payment fees

Late payment fees apply any time that you make a payment after your credit card’s due date. These fees will kick in even if your payment is late by a few days and you make payment in full. The best way to avoid these fees is by making sure you track all of your cards due dates and make payments on or before that date. Additionally, if your payment is more than 60 days late your card issuer can implement a penalty APR which is much higher than your regular APR!

Cash advances

Some credit cards will allow you to borrow cash using your credit card. Cash advances are usually available at a higher APR. In addition to this they also add on a fee that is typically 3%-5% of the cash advance amount (this varies by card). Seeking other alternatives to get cash may be a better option to avoid these fees.

Balance transfer fees

Credit cards may also allow a transfer of a balance from one credit card account to another. This is helpful if you can transfer debt to a card that offers a lower APR because you will reduce your interest. However, fees of 3% – 5% can be charged on the balance you are transferring. It is important to assess what the dollar amount of these fees will be for you. This will help you determine if the balance transfer is worth doing; or if you you should use the money to pay down the credit card debt.

Foreign transaction fees

Some credit cards will charge a 2-3% fee when you make purchases outside the U.S. If you aren’t sure if your credit card charges these fees make sure to call and ask before going abroad. If you travel often, search for a debit card or a credit card that doesn’t charge foreign transaction fees.

Over-the limit fees

Over-the limit fees can apply if you go over your credit limit. Credit card issuers can only charge these fees if you agree to them ahead of time. To avoid them make sure you opt out when you are signing up for a credit card. This way your card will be declined if you go over the limit.

Remember banks are in the money making business and the way they do this with credit cards is by charging high interest and fees! Don’t be intimidated by all of these fees. Instead make sure you understand the true costs of credit cards, know when these fees kick in and how much they cost before moving forward with these types of transactions.

Credit card providers will typically advertise these as opportunities to save money. Then they provide disclosures about them that are too long to read! That is why it’s important to know this information so that we can know how it can impact our wallets.

44 Comments

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback:

Pingback: